Are markets ready for tokenised stocks’ global impact?

September 2025 Are markets ready for tokenised stocks’ global impact? Nasdaq has filed with the SEC to tokenise every listed stock by 2026. If approved,…

Digitalization continues to accelerate our everyday life, affecting people, businesses, governments and financial institutions. The Covid-19 pandemic acted as a catalyst that revolutionized the way people work, purchase, and invest. The hype around non-fungible tokens (NFTs) and decentralized finance (DeFi) is evidence of the growing interest in investment opportunities brought by blockchain technology. According to a recent report, security tokens are seen as the next blockchain wave and are predicted to reach a market of €918 billion by 2026.

Naturally, the demand for these new means of investment has pushed digital money into the spotlight. Why? Because the cash leg must be on the same infrastructure as the securities in order to allow a real transition to a decentralized network. While most banks are still waiting for central bank digital currencies (CBDCs) to show the way, stablecoins issued by crypto players have reached a record-high trading volume at $766.02 billion in May, up 51.9% from the previous month, and nearly 15x greater than one year ago.

CBDC vs Commercial bank digital money vs Stablecoins:

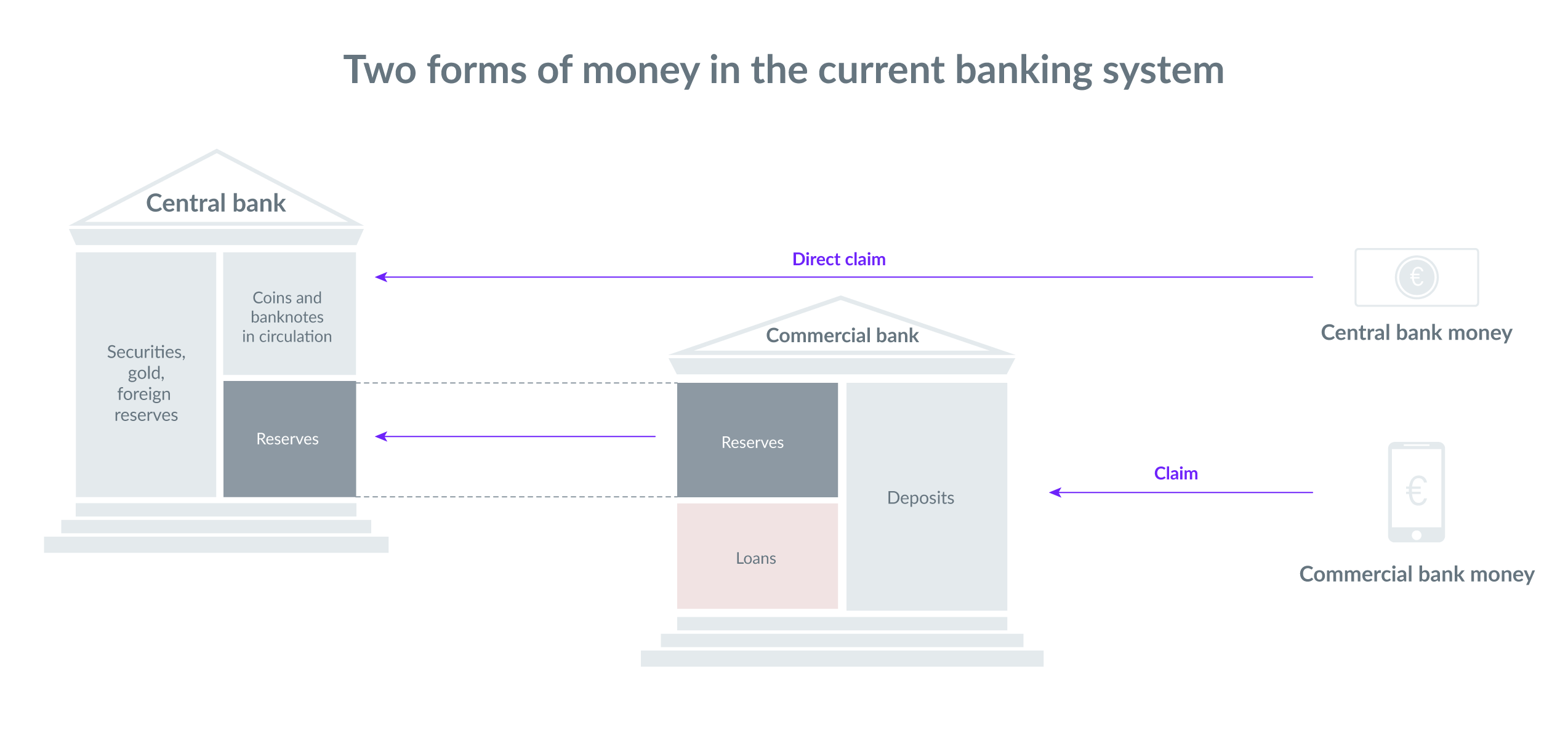

First, let’s take a deeper look at the two forms of money in the current banking system: central bank money and commercial bank money. Central bank money is made available to the public in the form of cash and to commercial banks in the form of central bank reserves. Private money is deposited into commercial banks, and banks are required to hold a certain percentage of these deposits at the central bank as a cushion. The rest of the deposits are used to grant loans to individuals and companies, where commercial bank money is created at this point. Therefore, in traditional finance, commercial banks act like trusted entities to not only provide essential services to customers, but also help create capital and liquidity in the market.

Similarly, stablecoins require promise and credibility, and they must be interchangeable with existing forms of money, in other words, they have to be anchored. This means stablecoins require users to have the same level of confidence as commercial bank money. Therefore, in onchain finance, commercial banks must take this role of trusted issuer of tokenized cash as they are the most suitable entities to issue stablecoins anchored by fiat money. They have already missed the ecommerce revolution to payment giants such as Stripe, Adyen, and Alipay, and have lost significant retail market share to neobanks. Will this happen again in the digital currency revolution?

Banks are at a critical juncture for catching up with this new wave. If they don’t act quickly, they will be seriously disrupted. With the emergence of crypto players such as Circle (which just reraised $440M), Paxos (which is now a bank), and our partner Monerium (a fiat-eMoney payment gateway for security token investors), the race is already on to become the tokenized money provider for digital assets.

As a reminder, with Tokeny’s platform you can:

Digital Identity, The Key For Security Token Custody

Digital identities lie at the heart of security tokens custody for investors, and secure the assets against loss and theft.

Why Have Binance’s Stock Tokens Concerned Regulators?

Binance has declared that holders of their stock tokens will qualify for economic returns on the underlying securities, including potential dividends, making the tokens securities.

The T-REX Billboard Explainer Video

A white-label secondary market solution for security tokens

The Security Token Report 2021

The 93-page report carefully curates industry expertise from 13 authors in six countries, including Tokeny Soltuions, all of whom work at the forefront of this capital market evolution.

Cointelegraph

EcoWatt Becomes the First Green Asset-Backed Store of Value on the Blockchain

EcoWatt puts renewable energy assets on the blockchain to disrupt the climate change movement by making green assets accessible to the blockchain community.

The Tokenizer

Crypto Startup Circle Is Said to Evaluate Potential SPAC Deal After $440M Fundraising Round

Crypto startup Circle, the company behind USD Coin (USDC-USD), raised $440M in a funding round and the company is said to be considering a SPAC transaction.

Seeking Alpha

Paxos Becomes Third Federally Regulated Crypto ‘Bank’

Paxos earns a provisional trust charter through the U.S. Office of the Comptroller of the Currency.

Coindesk

Deutsche Bank and Singapore fintech STACS complete ‘bond in a box’ proof-of-concept on the use of DLT for digital assets and sustainability-linked bonds

Deutsche Bank Securities Services in Singapore and Hashstacs Pte Ltd (‘STACS’) announced the completion of their proof-of-concept (‘POC’) referred to as “Project Benja”.

Deutsche Bank

Sweden’s Central Bank to Test Digital Currency With Handelsbanken

The Riksbank will partner with Handelsbanken to test how the e-krona might work in the real world.

Coindesk

ECB Says Lack of Official Digital Currency Risks Loss of Control

Countries that decide not to introduce digital versions of their currencies may face threats to their financial systems and monetary autonomy, the European Central Bank warned.

Bloomberg

Standard Chartered, OSL Parent in Pact to Create Digital Assets Platform

Initially targeting the European market, the U.K.-based company will seek to connect institutional traders to counterparties across markets.

Coindesk

Singapore Rolls Out World’s First Asset-Backed Digital Token Exchange

Cyberdyne Tech Exchange (CTX) of Singapore announced itself as the world’s first regulated digital exchange for tokens backed by real assets, fully live and open for business.

Investable Universe

It’s Official: El Salvador’s Legislature Votes to Adopt Bitcoin as Legal Tender

A supermajority of the El Salvadoran legislature voted to adopt bitcoin as legal tender early Wednesday morning.

Coindesk

Security Token Offerings (STOs) for NFTs?

Thinking of selling NFTs? If so, you should be aware that the issuance of NFTs may, in some circumstances, constitute the sale of securities.

Dilendorf Law Firm

Thailand SEC seeks to regulate decentralised finance

Activities related to decentralised finance (DeFi) projects which involve digital coin issuance may require a licence from the regulator in the near future, the SEC announced.

Bangkok Post

A monthly newsletter designed to give you an overview of the key developments across the asset tokenization industry.